Register now, make more friends, enjoy more functions, and let you play in the community easily.

You need Sign in Can be downloaded or viewed without an account?Register Now

x

brief introduction:

This strategy adopts a dual currency price difference to expand and narrow profits, and entry coordination includesRSIThe combination of extreme value and high success rate, using the idea of layered liquidation and exit, generates a large number of profitable orders every day and will not be trapped. Whether it's brushing orders or earning price differentials, it's a great choice. The most popular, safe, and stable profit method in today's trading world is hedging arbitrage. Based on the R&D philosophy of minimizing risk control and maximizing profits, it abandons the traditional idea of overnight wealth, allowing investors to obtain long-term stable returns while ensuring safety.

EAThe only drawback is that there will always be a slight loss, not very attractive, and may not be suitable for those who have a habit of cleanliness. Those who truly want to make money should focus on net worth rather than whether there is a floating loss on the balance.

We have designed a dual currency arbitrage model based on the inherent linkage of currencies:GBPUSD&GBPCHF arbitrage model .because GBPUSD&GBPCHFThe correlation coefficient of is95.86% Most of the time, their trend tends to be consistent.

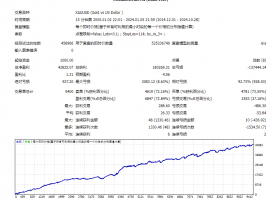

As shown in the following figure:

The essence of our price difference regression arbitrage is to summarize the laws of historical prices and form a combination, such as:USDJPY&CHFJPY

Below:

Multiple currenciesAemptyB perhaps manyBemptyA Historical maximum and minimum values Then obtain the mean, and when the price difference deviates significantly from the mean, there is a demand to return to the mean.

(1)If the price difference is greater than the average at this point, we will short this combination.

(2)If the price difference is less than the average at this point, we will go long on this combination.

When the price difference returns to the mean, these regression points are the overall return of our portfolio.

The higher the frequency of mean regression, the more trading opportunities there are. Entering the market far from the mean and returning to the mean, the greater the points of return. When the market changes and the price difference no longer returns to the mean, we need to stop losing or abandon this model.

From the mean chart above, it can be seen that although the frequency of mean regression is high, the amplitude of regression is not significant and cannot achieve profitability. So although these two currency pairs have strong correlation, this model is not suitable for arbitrage

We can see that these five combinations have roughly the same trend.

WhenGBPUSD&GBPCHFRegression mean, orUSDJPY&CHFJPYRegression mean,NZDUSD&AUDUSDRegression mean,EURUSD&NZDUSDRegression mean,EURUSD&AUDUSDReturn to the mean, you can make a profit! This increases the frequency of mean regression and also increases returns.

|

"Small gifts, come to Huiyi to support me"

No one has offered a reward yet. Give me some support

|

【顺势突破】黄金智能交易系统

这不是一套依靠重仓搏单边的“暴力EA”,而是一套极其稳健且逻辑清晰的趋势突破策略。

【顺势突破】黄金智能交易系统

这不是一套依靠重仓搏单边的“暴力EA”,而是一套极其稳健且逻辑清晰的趋势突破策略。

Aurra Markets:【欧元兑美元走势分

欧元兑美元的反弹是多头陷阱,还是趋势反转信号?在美联储决定维持利率不变后,欧元

Aurra Markets:【欧元兑美元走势分

欧元兑美元的反弹是多头陷阱,还是趋势反转信号?在美联储决定维持利率不变后,欧元

Aurra Markets:亚马逊第二季度营收

亚马逊 2026 年第二季度的业绩表现如何?亚马逊在2026年第二季度交出了令人瞩目的营

Aurra Markets:亚马逊第二季度营收

亚马逊 2026 年第二季度的业绩表现如何?亚马逊在2026年第二季度交出了令人瞩目的营

【无敌黄金】一单一结

bookEAbyMT4平台专属现货黄金自动化交易程序,核心采用严格一单一结机制,同一时段仅持

【无敌黄金】一单一结

bookEAbyMT4平台专属现货黄金自动化交易程序,核心采用严格一单一结机制,同一时段仅持

Aurra Markets:【白银走势分析】银

Silver breakthrough 60 美元后的涨势能否持续?白银(XAG/USD)近期出现大幅跳空上涨,主要受

Aurra Markets:【白银走势分析】银

Silver breakthrough 60 美元后的涨势能否持续?白银(XAG/USD)近期出现大幅跳空上涨,主要受

Riser card

Riser card Top card

Top card Silence card

Silence card Color changing card

Color changing card lifting jack

lifting jack